As worries over impending fiscal disasters have ebbed, funds continue to flow into stock markets. On a grand scale of total market valuations, or in comparison to 2008 outflows near $416 billion, the current inflows of $66 billion don't seem significant. About half of this great flow of funds appear to be going into international and emerging market funds, instead of into US listed equities. The continued low yield on bonds has failed to attract investors, so the theory of this latest flow data is that investors are now once again confident in stock markets and looking for some gains. The contrary indicator in all this, as mentioned in that video link above, is that large inflows have historically occurred near market tops. As Jason Zweig of the Wallstreet Journal points out, large institutional investors are also participating in the increased inflow of funds. As the so-called "Great Rotation" continues, another trend has appeared as funds have gone into Exchange Traded Funds (ETFs) that cover debt instruments, emerging market bonds, and other fixed income. The attraction of some of these ETFs is the steady payout ratio, combined with a perception of less risk than stocks or stock based funds.

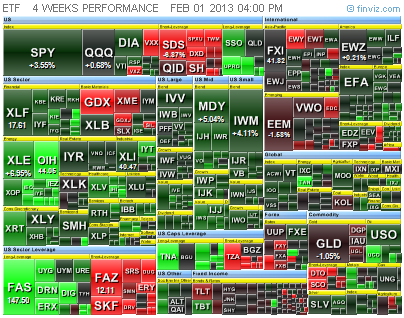

The idea that individual investors are driving market gains does not appear to be that convincing. January is historically an important time for fund managers to reposition portfolios, so under somewhat normal market conditions, we can expect inflows. Even with ETFs, it's important to remember that the managers of many of these funds buy and sell stocks to cover the investment portfolio identified in the prospectus. Despite analysts identifying some trends, when we look at the gains over the last four weeks, we can see that energy ETFs have performed well, though long and leveraged funds have performed even better. Just on a supply and demand basis, it appears that some complacency has set in. When we look at volatility (VXO)(VIX) indexes, we find they are at historically low levels. The long term volatility level of the S&P 500 is closer to 20 on the VIX. A trend we see emerging on VIX Futures indicates major investors expect the VIX to rise over the next few months. Usually movements in the VIX are opposite movements in the S&P 500, so if these futures positions prove to be correct, then we can expect a slow decline in the stock market. Instead of a Great Rotation from bonds to stock, it may be more a case of funds that were on the sidelines, either in money market funds or cash, now being used to purchase equities. Sales of new issuance of 5 year US Treasuries in January were well subscribed, and the yield on the 10 Year US Treasury has barely crept upwards. In all this it is important to remember that sometimes fund flows correlate with market gains, while other times there is an inverse correlation. As we continue through earnings season, it is important that companies continue to meet or beat earnings estimates. If the fundamentals continue to look strong, then equities could continue to rise. One thing to watch in earnings reports is forward guidance, though we may see a new precedent in guidance after insurance company Ace Ltd. (ACE) Ceo Evan Greenburg questioned the idea of giving guidance.

The idea that individual investors are driving market gains does not appear to be that convincing. January is historically an important time for fund managers to reposition portfolios, so under somewhat normal market conditions, we can expect inflows. Even with ETFs, it's important to remember that the managers of many of these funds buy and sell stocks to cover the investment portfolio identified in the prospectus. Despite analysts identifying some trends, when we look at the gains over the last four weeks, we can see that energy ETFs have performed well, though long and leveraged funds have performed even better. Just on a supply and demand basis, it appears that some complacency has set in. When we look at volatility (VXO)(VIX) indexes, we find they are at historically low levels. The long term volatility level of the S&P 500 is closer to 20 on the VIX. A trend we see emerging on VIX Futures indicates major investors expect the VIX to rise over the next few months. Usually movements in the VIX are opposite movements in the S&P 500, so if these futures positions prove to be correct, then we can expect a slow decline in the stock market. Instead of a Great Rotation from bonds to stock, it may be more a case of funds that were on the sidelines, either in money market funds or cash, now being used to purchase equities. Sales of new issuance of 5 year US Treasuries in January were well subscribed, and the yield on the 10 Year US Treasury has barely crept upwards. In all this it is important to remember that sometimes fund flows correlate with market gains, while other times there is an inverse correlation. As we continue through earnings season, it is important that companies continue to meet or beat earnings estimates. If the fundamentals continue to look strong, then equities could continue to rise. One thing to watch in earnings reports is forward guidance, though we may see a new precedent in guidance after insurance company Ace Ltd. (ACE) Ceo Evan Greenburg questioned the idea of giving guidance. There is some concern that central bank actions are fuelling a currency war, which could hurt trade. Currently the United States and the European Union are working on a Free-trade agreement. If talks are successful, the economies of both regions would benefit. There is some urgency in accomplishing this, before India and China can establish a free-trade region. There would be a boost to GDP under such an agreement, with estimates for Europe's GDP to rise as much as 0.52% annually. After an off-hand comment from French Labour Minister Michel Sapin in which he described France as "totally bankrupt", it would appear that some agreement sooner, rather than later, would be very beneficial. Sapin also stated that France is very solvent though the country needs to continue to make progress on deficit reduction. A free-trade agreement would also help the United States, where GDP grew only 2.2% in 2012, and GDP fell 0.1% in the fourth quarter of 2012. The greatest declines in fourth quarter US GDP were from exports, private inventories, and government spending. That last one is interesting, in that decreased government spending would improve government debt levels, though that money would come out of GDP. If all other areas of GDP growth were positive in the US, then reduced government spending would not have too large a negative effect on GDP. Remove that spending too quickly, or when GDP growth is low, then the US could experience a large slowing of the economy. Many countries know they need to reduce deficits, but the trick is to do that in a way that does not stagnate an economy, nor throw an economy into recession.

There is some concern that central bank actions are fuelling a currency war, which could hurt trade. Currently the United States and the European Union are working on a Free-trade agreement. If talks are successful, the economies of both regions would benefit. There is some urgency in accomplishing this, before India and China can establish a free-trade region. There would be a boost to GDP under such an agreement, with estimates for Europe's GDP to rise as much as 0.52% annually. After an off-hand comment from French Labour Minister Michel Sapin in which he described France as "totally bankrupt", it would appear that some agreement sooner, rather than later, would be very beneficial. Sapin also stated that France is very solvent though the country needs to continue to make progress on deficit reduction. A free-trade agreement would also help the United States, where GDP grew only 2.2% in 2012, and GDP fell 0.1% in the fourth quarter of 2012. The greatest declines in fourth quarter US GDP were from exports, private inventories, and government spending. That last one is interesting, in that decreased government spending would improve government debt levels, though that money would come out of GDP. If all other areas of GDP growth were positive in the US, then reduced government spending would not have too large a negative effect on GDP. Remove that spending too quickly, or when GDP growth is low, then the US could experience a large slowing of the economy. Many countries know they need to reduce deficits, but the trick is to do that in a way that does not stagnate an economy, nor throw an economy into recession.The Federal Open Markets Committee of the Federal Reserve met recently and announced that the current program of $85B (billion) per month of quantitative easing (QE) will continue. The Wallstreet Journal runs a Fed Statement Tracker that compares the previous FOMC announcement to the current announcement. We can note that while there has been growth in economic activity and improvements in employment, there have also been disruptions. The Fed expect a continuation of steady economic growth at a "moderate pace". The Fed will continue to purchase longer term US Treasuries at the rate of about $45 billion per month, and purchase mortgage backed securities (MBS) at the rate of $40 billion per month. In the latest ADP Private Payrolls report, employment increased 192000 against an expectation of 165000. Personal incomes rose 2.6% in December 2012, while consumer spending only increased 0.2% indicating that many consumers are either saving or paying down debt. Both those figures are substantially down from 2011 levels. Contrary to the positive ADP Report, the Bureau of Labor Standards reported a rise in Initial Jobless Claims to 368k against an expectation of 350k. That leads us into January Non-Farm Payrolls at a slightly disappointing 157k against 160k expected, and an unemployment rate of 7.9%. Prior revisions for November and December added 127k new jobs. Despite these slightly mixed numbers and reports, we can add in a better consumer sentiment in the latest University of Michigan poll, with a reading of 73.8 against 71.5 expected. There were other slightly positive economic reports released Friday 1 February 2013, all of which added to a positive day on the stock markets.

As the vacancy rate has declined to 4.5%, renting has become more expensive in some parts of the United States. The average nationwide rent was $1048 in Q4 2012. According to Deutsche Bank the ratio of rent to after tax mortgage payments is now 107.8% on average. As we saw with Blackstone Group purchasing more properties to use as rentals, now we see some builders increasing the pace of apartment projects. Argus Market Research note that the Federal Reserve of Cleveland measured Median CPI (consumer price index) to be 2.3% to 2.4% throughout 2012. Median CPI is a different way to measure CPI, avoiding the computational and methodological ways normally used for CPI. Additionally, Owner's Equivalent Rents rose about 2% through 2012, indicating sheltering costs increases. The Bureau of Labor Standards (BLS) Rent Index increased 2.7% in 2012, and CoreLogic Research indicate that house prices surged 6.3% through October 2012. When we compare that to the 2.6% increase in personal income, we find that there are slight inflation pressures starting. This will be one area to watch in 2013, though for now inflation rising faster than CPI is not a good trend.

G. Moat

Disclosure: I hold positions in Euro futures and some European Sovereign Bonds through the Fisher-Gartman Risk Off ETN (OFF). This article is not a recommendation for investors to either buy, nor to sell, shares in OFF. Investors are advised to perform their own research prior to making investment decisions.